Key takeaways:

- A series of new economic forecasts from Indeed Hiring Lab suggest that in 2026, job openings are poised to stabilize, but may not grow much; unemployment is likely to rise, but not alarmingly so; and GDP growth looks to remain positive, but somewhat anemic.

- Sustaining current GDP growth in 2026 may depend on the ability of high-income households to continue to spend at elevated levels.

- If immigration policy continues on its current path, we can expect labor supply to remain tight in a variety of fields, including construction, hospitality, engineering, and medicine.

- If hiring remains strong in healthcare, and job creation continues in line with rates observed in recent years, job openings could remain relatively high and unemployment could remain low, especially if conditions improve in other sectors.

- If the mismatch in skills and experience between the jobs that are available and the workers that are available to fill them persists, hiring is likely to remain stagnant, and unemployment duration is likely to remain long.

- Federal worker layoffs and funding cuts have yet to meaningfully move the unemployment rate or GDP, but the recent weakening of the labor market and rising “low-hire” environment suggest that pressures are growing.

- Regional dynamics matter: In 2026, where you live and what you do will matter for your professional prospects at least as much as movements in top-line national trends.

Economic and labor market uncertainty is everywhere. The longest federal government shutdown in history has only recently ended, tariff policy remains unsettled, immigration continues to decline, monetary policy is in flux, and the labor market feels distressingly stuck in place. It’s no surprise that the Economic Policy Uncertainty Index hit record levels in 2025. Making matters worse, missing and/or delayed government data releases make assessing true economic conditions more difficult.

Difficult, but not impossible. Indeed’s world-class and near-real-time data offers a unique view of the market unavailable anywhere else. Hiring Lab economists have parsed that data extensively for indications of what conditions may look like in 2026 if and when the fog of uncertainty lifts. New this year, Indeed’s proprietary data was combined with dozens of professional forecasts and a deep understanding of historical economic relationships to estimate where GDP growth, the unemployment rate, and job openings are expected to stand at the end of 2026. The data suggest that job openings are poised to stabilize, but may not grow much; the unemployment rate is likely to rise, but not alarmingly so; and GDP growth looks to remain positive, but somewhat anemic. In short, don’t expect much movement one way or another.

But there are a variety of factors that will drive the ultimate numbers up or down — including the strength of consumer spending, changes to immigration policy, how concentrated growth is, ongoing changes to federal spending, and regional strengths and weaknesses. Nobody knows exactly how these trends will evolve over the coming year, but we can make some educated assumptions based on what we know today.

This report establishes our consensus, upside, and downside scenario forecasts for 2026 and examines the major trends we tracked throughout 2025, and how they’re likely to shape the year ahead.

Scenario planning: How unemployment, labor demand & economic growth could unfold in 2026

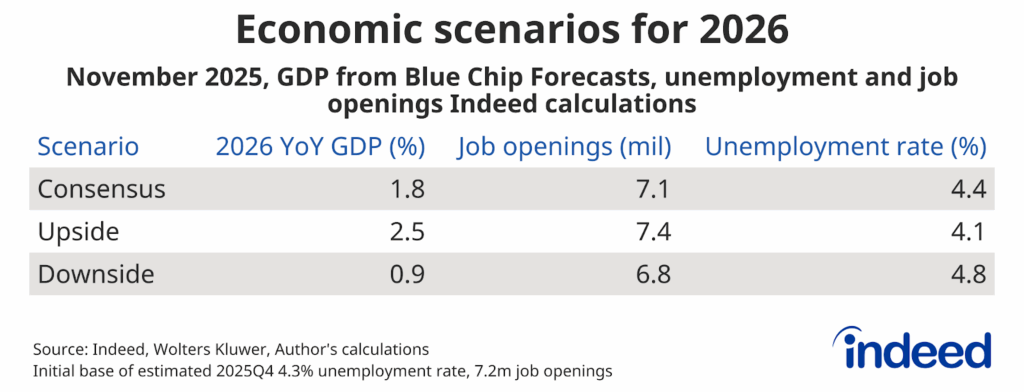

Hiring Lab constructed consensus, upside, and downside scenarios that estimate the unemployment rate and the level of job openings at the end of 2026. These scenarios were informed by Wolters Kluwer’s Blue Chip 2026 GDP growth forecasts, an aggregation of forecasts from economists and financial professionals.

The Blue Chip Consensus Scenario is derived from Blue Chip’s November 2025 consensus forecast for 2026 real GDP growth, which averaged 45 economist forecasts. For the Upside Scenario and Downside Scenarios, we use the average of the top ten and bottom ten forecasts for real GDP growth, respectively. It is important to note that these do not represent the best and worst case scenarios for the economy; instead, they are illustrative of slightly more positive and negative outlooks than the consensus average. From these GDP growth forecasts, we then used known historical relationships between economic growth and labor market performance to estimate both the unemployment rate and the number of job postings at year-end 2026. Further details can be found in the methodology section at the end of this report.

The Blue Chip consensus forecast for real GDP annual growth in 2026 is currently 1.8%, with the top 10 and bottom 10 forecasts averaging 2.5% and 0.9% growth, respectively. This then translates into estimated unemployment rates ranging from 4.1% to 4.8%, and job postings levels ranging from 6.8 million to 7.4 million at the end of next year. Interestingly, both the current unemployment rate and level of job postings are within this range and close to the consensus scenario. This indicates that, on average, big economic swings are not anticipated by the consensus in 2026.

The consensus scenario would indicate that the current “low-hire, low-fire” labor market, in which employers are unsettled enough about the economic outlook to punt hiring decisions but not concerned enough to make significant layoffs, is likely to continue.

The upside scenario would indicate a labor market taking a turn for the better, most likely precipitated by a clearing of uncertainty around immigration, tariff and monetary policy, a rebound in consumer sentiment, and further reductions in inflation. This scenario would likely accompany a pickup in the hires and quits rate as firms increase hiring and more workers take advantage of rising opportunities in the labor market to switch roles.

If uncertainty persists and consumer sentiment remains weak, then the downside scenario is more likely. Employers still looking to hire would very likely see a substantial increase in candidate volume due to the decline in job postings. This could be mildly tempered by a drop in the labor force participation rate as workers fall out of a discouraging labor market. Some industries could be hit especially hard.

Each of the following dynamics is likely to influence economic conditions to some degree, and each will in turn be shaped by how the broader labor market evolves. How these trends unfold — whether they hold steady, improve, or deteriorate — will help determine which scenario best describes the economy at the end of 2026.

Labor demand slowed, but GDP growth was solid. Can it stay that way?

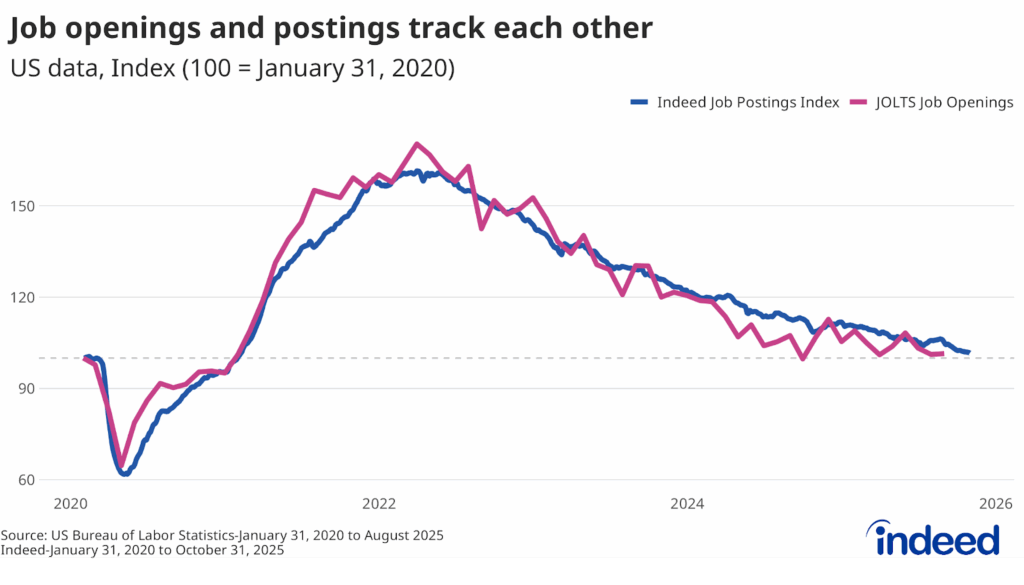

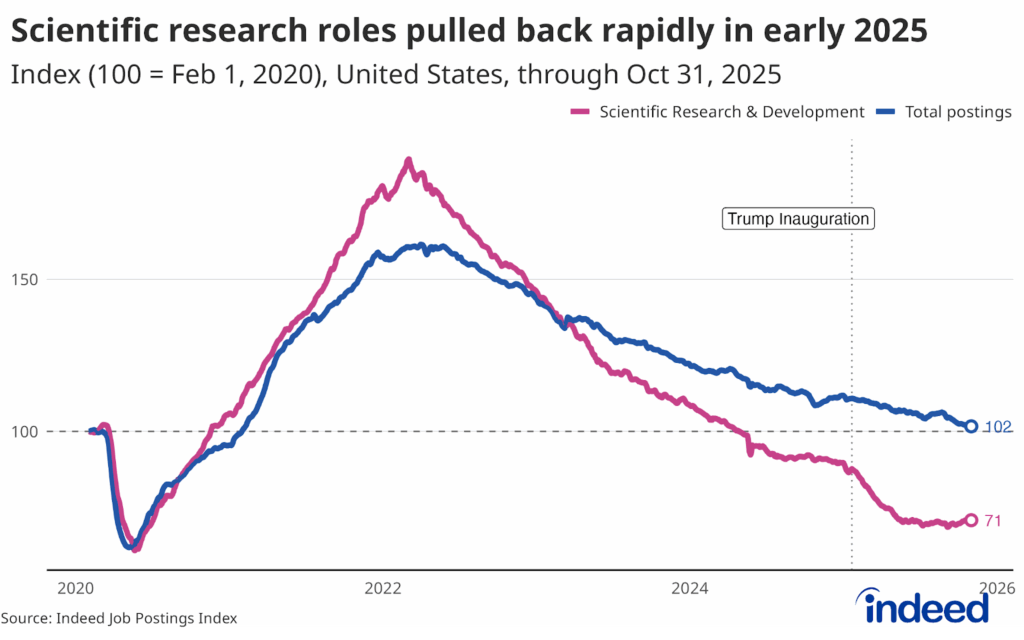

Overall hiring demand and the subsequent pace of hiring cooled consistently throughout 2025, leading to slower wage growth, declining labor force participation, and longer job searches for unemployed workers. Indeed’s Job Postings Index (JPI) is a real-time measure of employer demand based on the level of job postings on Indeed at any given time. Readings above 100 indicate that demand is higher than it was prior to the pandemic, and readings below 100 indicate that demand is lower than pre-pandemic levels. On New Year’s Day 2025, JPI was more than 10% higher than pre-pandemic norms (an index reading of 111.7). By the end of October, it had fallen to less than 2% above pre-pandemic levels (an index reading of 101.7). This closely follows the trends reported by the Bureau of Labor Statistics’ (BLS) JOLTS report.

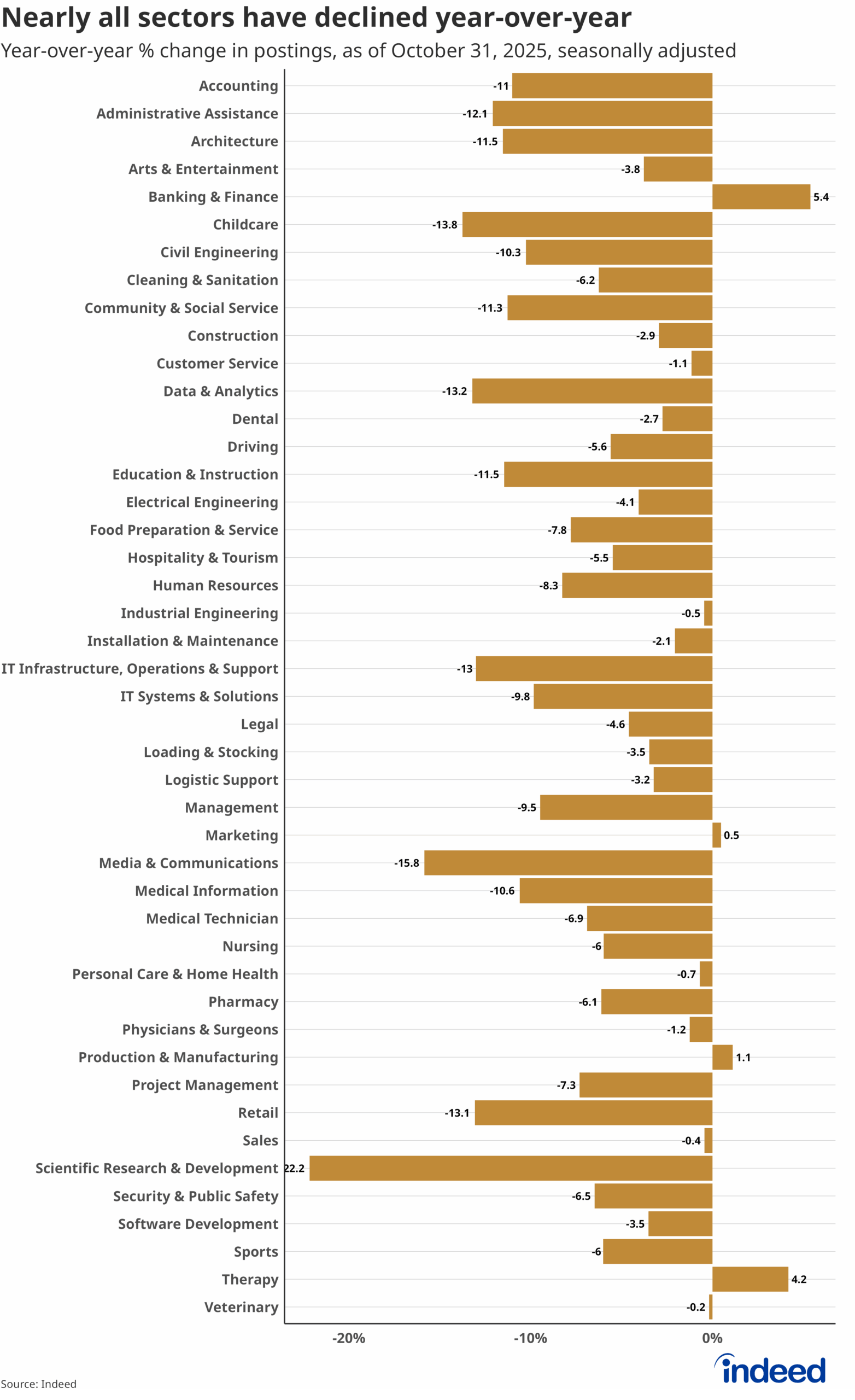

While demand has fallen from a year ago in virtually every professional sector tracked by Indeed, the cooling job market has been uneven, with demand in some sectors falling much more significantly than others. Job seekers looking for roles in fields with relatively high JPI levels, including civil engineering (154.0) and personal care and home health (148.4), will have a far different experience than those seeking work in harder-hit sectors, including media & communications (64.1) and scientific research & development (70.8).

But while the labor market continued to weaken throughout 2025, GDP growth has been surprisingly steady, defying expectations from earlier this year. Between March and April — when proposed economic changes first began to come into clearer view, including massive new tariffs and sweeping immigration and industrial policy changes — consensus Blue Chip 2025 forecasts for real, year-end GDP growth fell from 2.0% to 1.4%. On average, the lowest 10 predictions at the time called for annual GDP growth by year’s end of just 0.6%. But in the months that followed, many of the largest announced and proposed changes from the new administration were challenged, reduced, or even eliminated, and GDP remained more resilient than expected. In November, the same forecasts called for year-end GDP growth of 1.9% on average, with the bottom 10 forecasters expecting annual growth to end 2025 at 1.7%, both well above their April expectations.

Continued strength in consumer spending, which makes up roughly 68% of GDP, is a big reason for the sustained strength in GDP growth this year. Yet a growing, and disproportionate, share of consumer spending is coming from top income earners. A recent study from the Bank of America Institute indicated that spending by high-income earners grew 2.6% year-over-year in September. Over the same period, spending by middle- and low-income earners grew just 1.6% and 0.6%, respectively. The gap between spending levels of households of different income levels grew noticeably in 2025 and is much wider than has been observed in the post-COVID era.

For many families, wage and income growth play a significant role in their ability to increase spending. Wage growth as measured by the Indeed Wage Tracker, which tracks changes in advertised salaries in job postings, also slowed in 2025, to 2.5% year-over-year by September, down from 3.4% at the start of the year. This slowdown has been fairly widespread, with similar annual growth in advertised wages observed for high-, medium-, and low-paying roles. Annual wage growth of 2.5% is not wildly out of line with historic norms, so this broad slowdown is not overly concerning in a vacuum. The challenge today is that the annual pace of inflation is now running hotter than wage growth, which has serious implications for consumers’ purchasing power, especially for lower-income workers with less of a savings buffer.

With overall layoffs and the unemployment rate both still relatively low, this underlying weakness in consumption has not yet become a drag on GDP growth. But a deteriorating labor market in line with our adverse scenario may yet apply some pressure. If more people lose their jobs, or if it takes people significantly longer to find a job, consumption — and GDP with it — may take a hit.

Looking ahead at 2026:

- Sustaining the currently decent level of GDP growth in 2026 may very well depend on the ability of high-income households to continue to spend at elevated levels.

- It is possible, but less likely, that lower and middle-income households are able to increase their consumption more than expected.

- Growth in asset values, in everything from stocks to gold to cryptocurrency, will help determine how much spending can grow — especially in an environment where inflation remains elevated and the labor market remains soft.

Global talent in flux: What 2025’s immigration shifts could mean for hiring in 2026

This year has brought major shifts in immigration policy and enforcement. While several measures have already disrupted foreign talent flows, we have yet to see the full impact of recently announced policies, many of which have the potential to influence labor market conditions and recruitment strategies.

Over the past year, there has been a rise in detentions and deportations of unauthorized migrants, and several programs that offered temporary work authorizations for migrants from specific countries were terminated. More than a million people lost their legal status this year, and a large proportion also had their work permits revoked. While many of these individuals have not been deported, their ability to work legally in the US has been impacted significantly, and a fear of further enforcement may also be influencing these workers’ employment choices. Asylum restrictions and more stringent border control measures also served to drive down the number of migrants entering the country. Taken together, these developments will all have a direct impact on sectors that have traditionally been heavily reliant on migrant labor, including agriculture, construction, cleaning, and sanitation.

While greater immigration enforcement may have most notably impacted hourly workers, new policies will also affect professional workers. In September, the administration announced a one-time, $100,000 fee for new H-1B visa beneficiaries, the most common visa pathway for high-skilled immigrants and international students, especially in STEM fields. While the exact policy details remain uncertain, the changes are likely to significantly disrupt the pool of highly trained professional talent in fields including tech, engineering, and medicine. The full extent of the impact will not be observed until March 2026, when the FY2026 application period ends.

There has also been a drastic drop in the number of international students enrolled in US colleges and universities. A disproportionate number of international students come to the US to attain advanced degrees in STEM fields and subsequently join the workforce after their graduation. The recent decline in international enrollment signals another potential future shortfall in highly skilled talent for key industries.

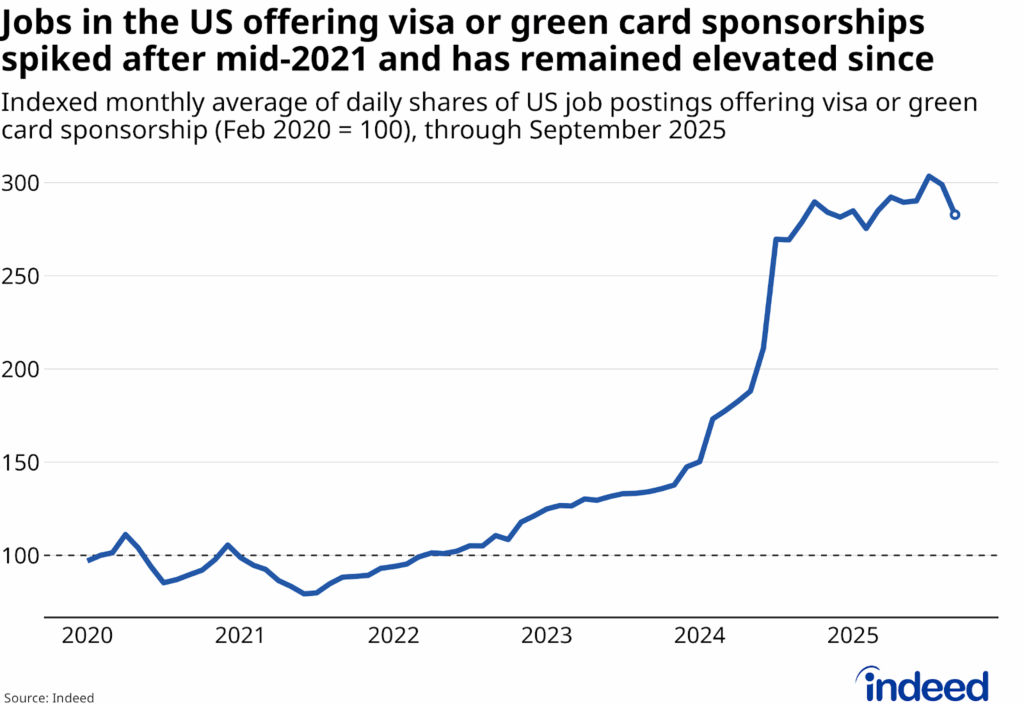

Indeed data reflects some of the impacts of these changes to immigration policy. The share of job postings that explicitly offer visa sponsorship remains elevated at almost three times the pre-pandemic share, with most of them coming from medical fields. This highlights both the ongoing labor shortages in the sector and the recognition and willingness of employers to turn to migrants to help fill them.

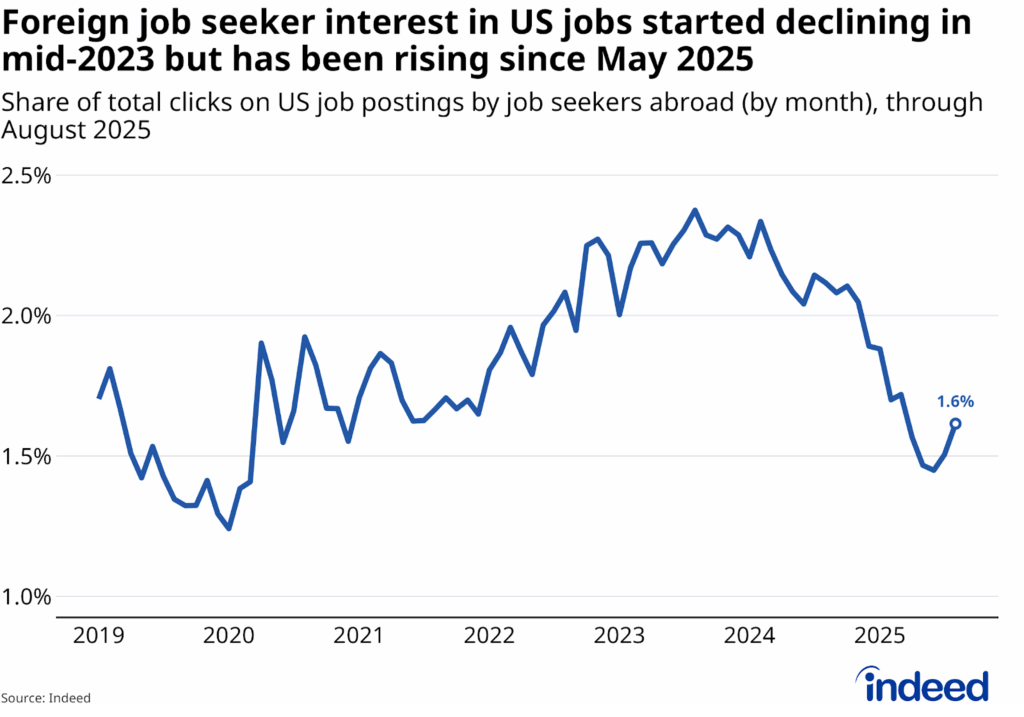

But even as employers extend a welcome, foreign job seekers’ interest in jobs in the United States has dropped, reaching an almost five-year low of 1.45% in June 2025. While the share has rebounded slightly since then, it remains well below the recent peak of 2.38% in August 2023.

This puts US employers in an interesting situation. Despite increasingly restrictive immigration policies proposed by the administration, US employers are still willing to sponsor visas to fill critical shortages. However, the uncertainty and fear around immigration enforcement are likely dampening foreign job seekers’ interest in US-based jobs. Going into 2026, the interplay between employer demands for global talent and tighter legal pathways for immigrants will shape the US hiring landscape, especially in fields with heavy percentages of foreign workers.

Looking ahead at 2026:

- If immigration policy continues on its current path, we can expect labor supply to remain tight in a variety of fields, including construction, hospitality, engineering, and medicine.

- In the short term, a smaller migrant workforce could push the unemployment rate down, even as employers continue to have serious issues filling open roles.

- In the longer run, the trend could hamper employers’ ability to maintain desired production and output levels.

- Loosening even some immigration restrictions could contribute to employers feeling more confident in their ability to hire and expand, potentially pushing job openings up in line with the more upside economic scenario outlined above. But further restrictions may lead to further contractions in overall job openings, more in line with the downside case.

Non-healthcare sectors are sick. What happens if the illness spreads?

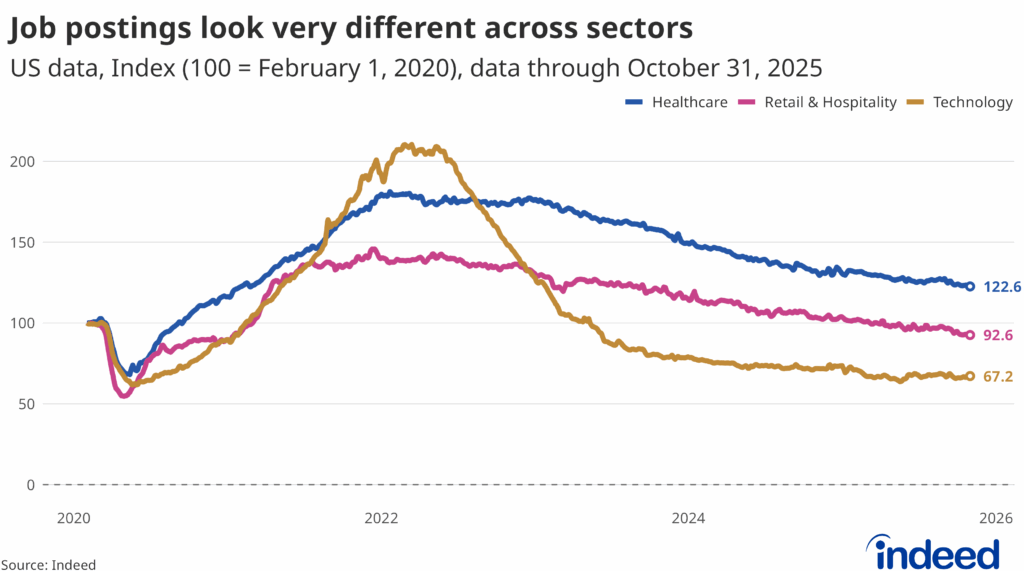

Job growth in 2025 has been heavily concentrated in healthcare — a sector largely insulated from broader economic cycles and clearly impacted by well-documented demographic shifts. As of August, healthcare accounted for just 11.4% of total US nonfarm employment, but represented 47.5% of all job growth recorded so far in 2025. As a result, discussions of the labor market must increasingly separate healthcare employment from the rest of the economy.

While headline job postings were 1.7% above pre-pandemic levels at the end of October, healthcare postings ended the month 22.6% above pre-pandemic levels. The healthcare, tech, and retail & hospitality sectors all experienced a strong post-pandemic boom in demand, but demand has since fallen off more quickly outside of healthcare. Postings in retail and hospitality are currently 7.4% below pre-pandemic levels, while tech job postings are almost a third lower than they were in early 2020.

Still, despite its recent strength, healthcare has not been immune to the overall weakening in demand that has characterized the market over the past year. Demand has declined year-over-year in virtually every sector tracked by Indeed, with 13 sectors falling by more than 10%.

In today’s “low-fire, low-hire” environment, those trying to enter the labor market in fields outside of healthcare (and a handful of other relatively high-demand fields, including civil engineering and construction) are bearing the heaviest burden. Young workers, in particular, are struggling — not because entry-level jobs have disappeared, but because employers are simply not expanding their workforce at the moment. While the number of junior positions has declined in absolute terms, these roles are not vanishing faster than job postings overall. In fact, in some cases, entry-level roles have remained steady — or even increased — as a share of total postings, despite the broader market slowdown. Put differently, the challenge for new graduates isn’t that junior roles are being uniquely squeezed out, but that the entire job market is contracting, leaving fewer opportunities across the board. This dynamic is reflected in the contrast between a low overall unemployment rate (but a decline in job postings) and monthly payroll employment growth. For those already employed, things may feel steady enough. But for those trying to break in — especially outside of the handful of better-performing sectors like healthcare — the landscape looks barren.

The 2025 labor market is best described as frozen, with the first signs of frostbite showing through. Employers and employees alike have so far weathered the freeze by battening down the hatches, with workers reluctant to leave their current jobs and businesses content to hang on to the workers they have without embarking on either hiring or firing sprees. Looking ahead to 2026, the question won’t be whether the market thaws — it will be whether it cracks.

Looking ahead at 2026:

- If layoffs begin to meaningfully increase next year, the freeze could quickly turn into a storm. History tells us that when layoffs increase considerably, higher unemployment rates are quick to follow.

- If hiring remains strong in healthcare, and job creation continues in line with rates observed in recent years, job openings could remain relatively high and unemployment could remain low, especially if conditions improve in other sectors. In this case, we could end up in the consensus, or even upside, scenario.

- Recent BLS data shows healthcare employment slowing, and job postings have declined year-over-year in each of the healthcare-related sectors tracked by Indeed. Continued erosion of labor conditions in healthcare, without serious improvements in other sectors, could move us toward the downside scenario.

Signs of mismatch: When available jobs don’t match available skills

As job postings have decreased, and the unemployment rate has increased, there has also been a significant shift in the average number of applications started per job posting, suggesting a mismatch between labor supply and demand. Indeed data indicate that while the number of applicants per job has declined by 75% or more in some sectors, others are experiencing application growth per job of more than 50%.

There are still a relatively high number of job postings in medical fields that require significant education, including for veterinarians and surgeons, but applications for roles in these fields are lower than they were two years ago. This suggests that while demand for talent remains high, the supply of interested candidates is not expanding at the same pace.

At the same time, the average number of applications per job has risen sharply for several blue-collar and service categories, including food prep and sanitation, a likely reflection of the ongoing realignment of the US labor market. As layoffs and uncertainty impact higher-skill occupations, many job seekers are likely to shift their focus to roles that offer steadier hiring and lower entry barriers. Quits rates for the healthcare and social assistance sector — including roles with both higher and lower applicant interest — are also slightly higher than the national average, adding to the varying retention challenges faced by different occupations within the sector.

The surge in interest for sectors including food service, cleaning, driving, and personal care may indicate workers are pursuing positions that remain in demand — as indicated by higher JPIs — despite broader economic changes. One exception is in the data & analytics sector, which had the lowest sectoral JPI of all sectors tracked as of the end of October (60.4), but a rising number of applications per job. This could be driven by a mismatch between demand and supply for these roles, caused by continued growth in new analytics workers and a rise in laid-off analytics workers, both of which are expanding the pool of candidates competing for a still-limited number of jobs.

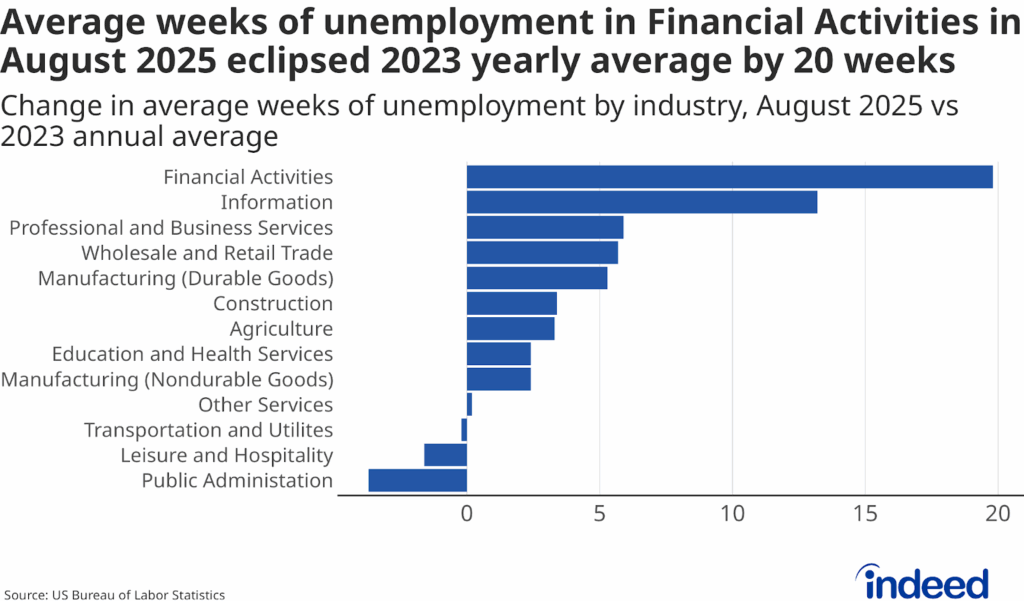

Changes in the time it takes for unemployed workers in various fields to find a new role can also help illustrate some potential misalignment between available jobs and available talent. Bureau of Labor Statistics data indicate that some of the largest increases in average unemployment duration since 2023 have been in white-collar fields, particularly financial activities, information, and professional and business services. The jump was especially dramatic in the financial activities sector, where unemployed workers spent about 20 more weeks searching for a job in 2025 than they did in 2023, the largest jump of any sector. Intriguingly, the sector also saw a much lower quits rate of 1.2% in the BLS data, as opposed to the country average of 1.9% in August 2025. Evidently, workers are reluctant to quit their current roles in the sector, as finding new roles is becoming increasingly challenging.

The fact that the sectors with the biggest increases in unemployment duration are also seeing the sharpest declines in applicants per job suggests that hiring in these fields has become significantly more selective. Even with fewer applicants competing for each open role, many job seekers are spending longer periods searching for a suitable match, possibly reflecting a growing mismatch between candidate backgrounds and employer requirements in these traditionally high-skilled sectors.

It should also be noted that unemployment duration has actually fallen in three sectors over the past two years: transportation and utilities, leisure and hospitality, and public administration. This may signal better matching between workers and employers, or it may simply reflect the lower skill requirements common in these fields.

Looking ahead at 2026:

- If job openings for highly skilled workers begin to grow meaningfully enough to bring more of these unemployed workers back into the job market more quickly, the labor market may move more in the direction of our upside scenario.

- But if the mismatch in skills and experience between the jobs that are available and the workers that are available to fill them persists, hiring is likely to remain stagnant and unemployment duration is likely to remain long, in line with the consensus or downside scenarios.

Funding freeze, hiring squeeze: The federal factor in 2026

Public sector employment sharply reversed itself in 2025, shedding 24,000 jobs between January and August. This represents a major departure from the one million net new jobs added in the sector in 2023 and 2024 (mostly in local government and education roles). Local government employment has increased by 104,000 jobs this year, but it hasn’t been enough to overcome sizable losses in federal and state government jobs, which have decreased by 97,000 and 31,000, respectively.

These losses are likely to grow as more data are released post-shutdown. Tens of thousands of federal workers reportedly accepted deferred resignations early this year, with many taking effect after August and not yet fully reflected in the available official data. And while the November agreement to reopen the government reinstated federal workers furloughed during the shutdown, additional reductions in force going forward cannot be ruled out, especially with another potential funding dispute looming in early 2026.

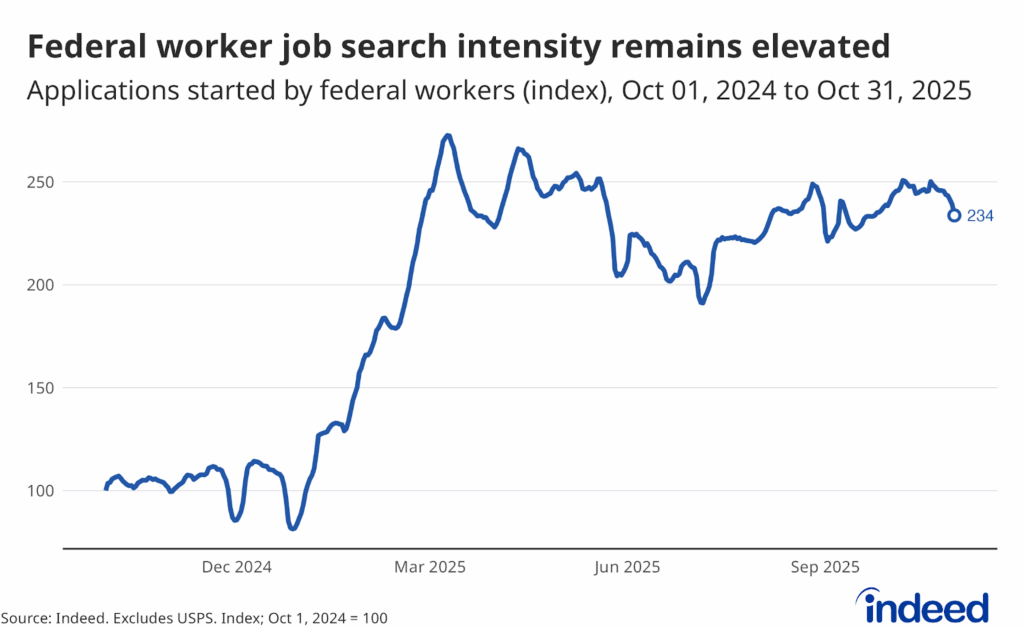

Amidst all these layoffs and uncertainty, federal workers have responded by seeking new employment opportunities. Job applications from federal workers surged early in the year, especially from workers in agencies then under review by the Department of Government Efficiency (DOGE). The early-year surge slowed somewhat in the spring, but applications began trending upward again in early July and remain almost 150% above their year-ago level by the end of October. The shutdown had a slight impact on the job search behavior of federal workers, with applications rising 8.5% month-over-month in October 2025.

Cuts and freezes in government spending have also directly affected hiring in certain non-government sectors, especially scientific research & development jobs. Job postings in this sector have slowed more quickly than overall job opportunities in recent years, but cuts to government research spending widened the gap further beginning in early 2025. On January 1, overall postings on Indeed were about 12% above their pre-pandemic levels, while scientific research and development jobs were 11% below. By the end of October, overall postings were 1.7% above early 2020 levels, but harder-hit scientific research & development sat 29% below their pre-pandemic baseline.

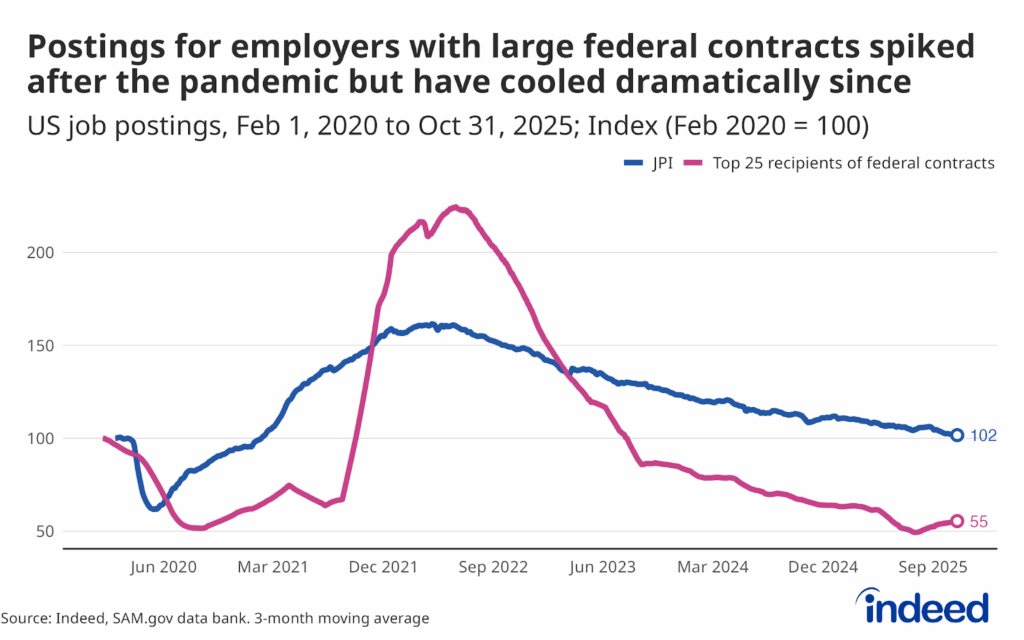

Federal funding reductions have also had a ripple effect on companies that rely heavily on government contracts. From January 1 to mid-July, hiring among the 25 employers with the most dollars received from government contracts pulled back by 23%, while the overall JPI decreased by 4.5%. Encouragingly, there have been signs of a rebound in federal contractor employment since mid-July, but there are still about 15% fewer opportunities with those companies now than there were when the year kicked off.

Employment with top contracting companies and the federal government remains relatively small, accounting for less than 5% of all jobs. But the reach of these jobs extends into many corners of the economy, and the spending, research, and social programs they help support have a wide impact on broader economic health and household stability. For that reason, government employment and spending will be key to watch for the health of the labor market and economy in 2026 and beyond.

Looking ahead at 2026:

- Federal worker layoffs and funding cuts have yet to meaningfully move the unemployment rate or GDP, but the recent weakening of the labor market and rising “low-hire” environment suggest that pressures are growing.

- Additional cuts to federal employment or funding going forward may lead to hiring challenges and could lead to higher unemployment and/or lower GDP, moving us closer to the downside scenario.

Location, location, location: The regional divide comes into focus

Ultimately, when we look at the economy as a whole, macroeconomic conditions at the end of 2026 will most likely end up somewhere between our upside and downside scenarios. But how the labor market feels to job seekers and employers is highly dependent on their sector and where their feet are planted. There is considerable variation in job posting levels across the country, with some states sitting well below their pre-COVID norms and others still showing elevated demand. As of the end of October, for example, JPI in Washington, D.C., was 65.0 (35 percent below pre-COVID levels, lowest among all states and territories), while job postings in Alaska were 51.1% above February 2020 levels. Depending on where you live, an upside scenario may feel like a downside scenario, and vice versa.

It is important to acknowledge the role migration plays in some of these local differences and dynamics. Many of the states with high JPI levels have also experienced relatively robust population growth, driven by cross-state migration, suggesting that increased consumer demand also drives employer demand. But in many states over the past five years, growth in job postings has exceeded population growth. In South Carolina, for example, job postings are 28.9 percent higher than in February 2020, while the state’s population is estimated to have grown only around 7 percent over the same time period. And in many of the states where the level of job postings relative to pre-pandemic norms is lower than the national average, postings are falling faster than changes in population. For example, in California, job postings are down around 17% compared to pre-COVID, while population growth estimates for the same period hover close to 0%. Clearly, job seekers will experience the labor market differently depending on each state’s underlying conditions.

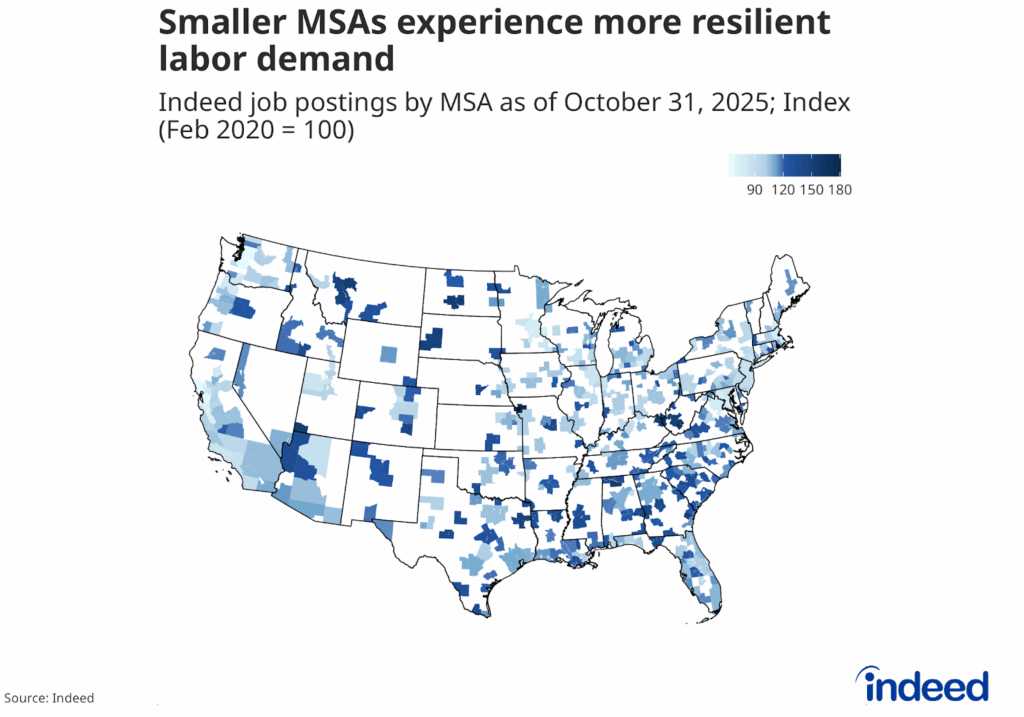

Variations in job postings are even more pronounced at the Metropolitan Statistical Area (MSA) level, where many of the strongest job markets are in the Sunbelt and Mountain West regions.

Interestingly, in nearly every state, the highest posting levels are found not in the largest MSAs, but in smaller and mid-size ones, where labor demand has proved more resilient. Take Georgia, for example. As of October 31, the JPI in Atlanta was 110, while the JPI in the smaller MSAs of Valdosta, Warner Robins, Macon, and Hinesville all exceeded 130. The same is true in Texas. JPI in Dallas and Houston stood at 105 and 111, respectively, at the end of October, while JPI in smaller MSAs, including Longview, Tyler, and San Angelo, was uniformly higher.

Overall, as of October 31, the average JPI in the nation’s largest MSAs (population estimates above one million) was 98.6. In contrast, mid-size MSAs (250,000 to 999,999 residents) averaged 112.0, and small MSAs (under 250,000 residents) averaged 115.5. Much of this is driven by sector diversification. Employment in many of the largest MSAs tends to be skewed towards tech, business, and professional services, which are seeing lower levels of job postings. Smaller MSAs, however, tend to have heavier employment shares in sectors, including manufacturing, leisure and hospitality, and healthcare, which generally have job postings that remain near or higher than pre-COVID norms.

As we move into 2026, much of the experience of both job seekers and companies looking to hire will depend on location. In smaller MSAs, labor supply will likely be tighter, and it may remain difficult to find workers with the skills employers are seeking. For job seekers in these locations and with the right skills, there may continue to be ample opportunities. But 2026 could remain an employers’ market in the largest MSAs. Job seekers, especially in non-healthcare-related fields, may have a more difficult time finding new employment opportunities.

Conclusion: Why 2026 will be different, but not unrecognizable

The labor market in 2026 is likely to feel different, but not unrecognizable. Across our consensus, upside and downside scenarios, unemployment, job openings, and GDP growth all remain within sight of where they are today — not too hot, not too cold, simply stable. The most probable outcome is not a dramatic break from current conditions, but an extension of today’s “low-hire, low-fire” environment in which both employers and job seekers face a slower, more selective market. The range of plausible outcomes is real, but so is the message from the data: big swings are unlikely.

But small changes in the aggregate can often feel like big changes around the margins. Demand has cooled from a year ago in nearly every professional sector, but the pullback has been uneven. Opportunities remain relatively plentiful in fields including civil engineering and healthcare, and in many small and mid-size MSAs, particularly in the Sunbelt and Mountain West. But job seekers in media, scientific R&D, and other harder-hit professional fields, and those in large coastal MSAs with slower population growth and more exposure to tech and professional services, are likely to face tougher conditions. In 2026, where you live and what you do will matter for your professional prospects at least as much as movements in top-line national trends.

The broader macroeconomic backdrop will also be defined by cross-currents. Consumer spending has so far kept GDP growth on solid ground, but it has increasingly been powered by higher-income households. Wage growth has cooled and inflation has eroded purchasing power for many lower- and middle-income workers. The full details and impacts of new tariff policies, immigration restrictions, and changes to federal spending are likely to remain uncertain for some time, and that uncertainty itself sits in the background of all our scenarios. Each of these forces has the potential to nudge the economy and labor market toward the upper or lower end of our forecast ranges, or, in the case of a particularly severe shock or beneficial breakthrough, beyond them.

For employers, this environment underscores the importance of being both disciplined and opportunistic. In tighter local or occupational labor markets, maintaining a competitive edge on pay, flexibility, and career development will remain critical to attracting and retaining talent. In areas or sectors where more candidates are chasing fewer jobs, employers may find an opportunity to raise the bar on hiring, invest in training, and rethink role design to better match evolving skills and business needs. For job seekers, a slower but still growing economy means that patience and persistence will be essential, as will a willingness to adjust search strategies — including where they look, which roles they consider, and which skills they choose to build.

This is a moment when timely, granular data matters more than ever. Official statistics will continue to provide an essential snapshot of where the economy is and has been. But in an era of heightened uncertainty and occasional data gaps, near real-time labor market information can help fill in the picture of where conditions may be headed. Indeed’s Job Postings Index, wage data, and local labor market indicators can give employers, job seekers, and policymakers a clearer view through the fog. We will continue to monitor these trends, refine our scenarios, and share new insights as the year unfolds.

Methodology

Our forecast scenarios were determined based on key assumptions about the relationship between a handful of economic variables:

- Forecasted GDP growth relative to potential GDP growth

- Sensitivity of the unemployment rate to GDP growth (Okun’s Law coefficient)

- Sensitivity of job openings to the unemployment rate (the slope of the Beveridge Curve)

The numbers included in our downside scenario can provide a good example. Real year-over-year GDP growth of 0.9% in 2026 would represent a 1.1 percentage point (ppt) shortfall compared to the Congressional Budget Office’s latest estimates of potential GDP growth (2%). Based on estimates of an Okun’s Law of 0.45 — every 1 ppt shortfall in GDP growth compared to trend is associated with a 0.45 ppt increase in the unemployment rate — this slower pace of GDP growth translates to a 0.50 ppt rise in the estimated unemployment rate, from 4.3% at the end of 2025 to 4.8% by the end of 2026.

That projected change in unemployment is then applied to the Beveridge Curve. Based on the estimated, longer-term -0.52 slope of the Beveridge Curve from 2010-2019 (excluding periods when unemployment exceeded 6%), the job openings rate declines 0.52 ppt for every 1 ppt increase in the unemployment rate. Therefore, the 0.50 ppt rise in the unemployment rate translates to a 0.26 ppt decline in the job opening rate. We estimate the job openings rate and job openings level to stand at 4.3% and 7.2 million, respectively, by year-end 2025. This means a 0.26 ppt drop would leave the job openings rate at 4%, and job openings at 6.8 million at the end of 2026.

The number of job postings on Indeed.com, whether related to paid or unpaid job solicitations, is not indicative of the potential revenue or earnings of Indeed, which comprises a significant percentage of the HR Technology segment of its parent company, Recruit Holdings Co., Ltd. Job posting numbers are provided for information purposes only and should not be viewed as an indicator of the performance of Indeed or Recruit. Please refer to the Recruit Holdings investor relations website and regulatory filings in Japan for more detailed information on revenue generation by Recruit’s HR Technology segment.