Bank of America estimates that by 2030, China’s capital expenditure in non-IT sectors such as power systems, cooling technologies, and critical metals will account for one-third of total AI investment, fostering a massive market valued at RMB 800 billion. By then, the direct copper demand from AI data centers in China alone is expected to reach approximately 1 million metric tons, representing 5-6% of China’s total copper demand at that time.

Author of this article: Long Yue

Source: Hard AI

The wave of artificial intelligence is not only about algorithms and computing power; behind it lies a race concerning energy and physical infrastructure. In addition to chips and servers, the power systems that fuel AI data centers, the cooling technologies that ensure their stable operation, and the metal materials required for construction are together forming a new investment domain.

The wave of artificial intelligence is not only about algorithms and computing power; behind it lies a race concerning energy and physical infrastructure. In addition to chips and servers, the power systems that fuel AI data centers, the cooling technologies that ensure their stable operation, and the metal materials required for construction are together forming a new investment domain.

According to a recent report released by BofA Global Research, the market size of China’s AI-related ‘non-IT’ infrastructure capital expenditure is expected to reach RMB 800 billion by 2030.

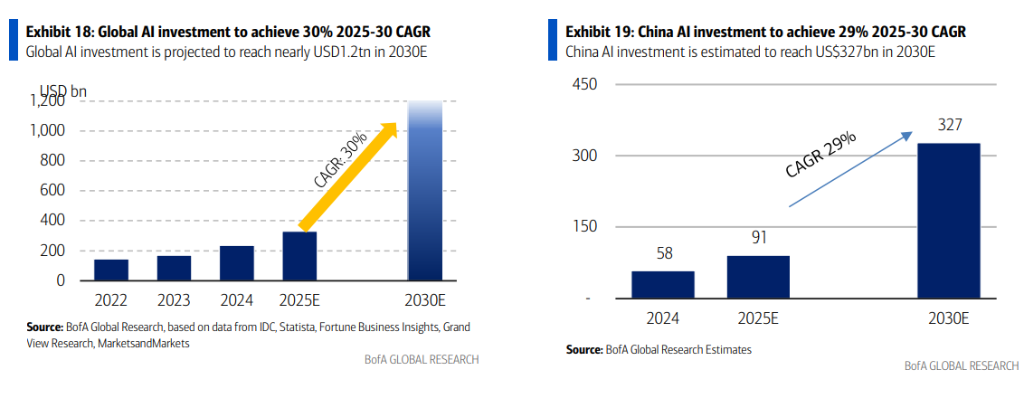

The report forecasts that global AI-related capital expenditure will exceed USD 1.2 trillion by 2030. Of this, China will play a key role, with its total AI capital expenditure growing from RMB 600-700 billion in 2025 to RMB 2-2.5 trillion by 2030, at a compound annual growth rate (CAGR) of 25-30%.

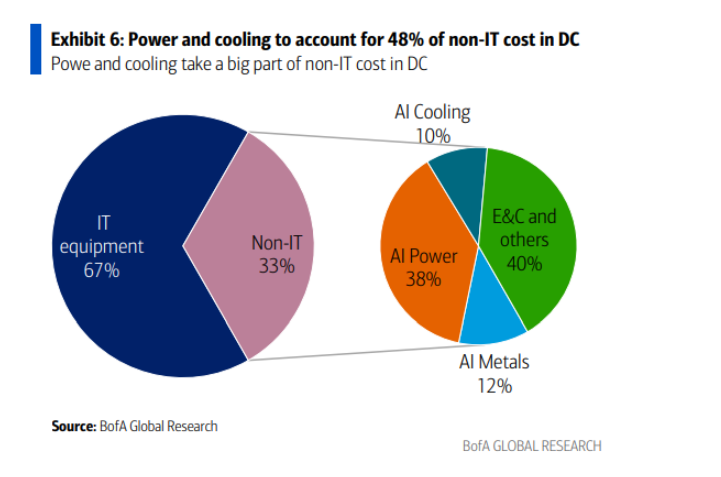

Energy supply is regarded as the cornerstone of AI development. Approximately one-third of these investments, amounting to RMB 800 billion, will be allocated to non-IT infrastructure supporting the operation of AI data centers. This includes power generation and transmission (38%), metals required for data center construction (12%), advanced cooling systems (10%), and other engineering projects.

This trend presents clear investment opportunities in areas such as nuclear power, grid equipment, energy storage, backup power supplies, and advanced heat dissipation technologies, which have already extended to upstream metal markets including copper, aluminum, and uranium.

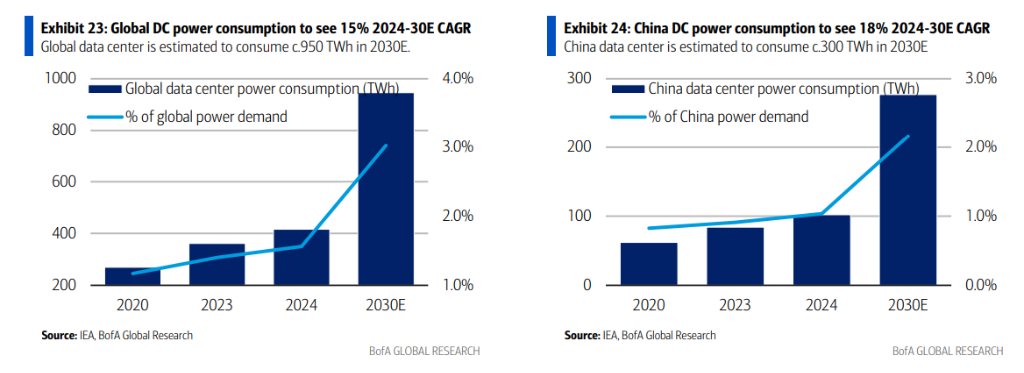

As demand for AI computing power grows explosively, the focus of the global AI race is expanding from computing power itself to energy. Data from the International Energy Agency (IEA) shows that by 2030, electricity consumption by China’s data centers is projected to increase from 102 terawatt-hours (TWh) in 2024 to 277 TWh, with an annual compound growth rate as high as 18%.

Powering AI: Five Key Opportunities Emerge

“Without electricity, there is no AI.”

The training and inference processes of AI models require immense computational power, which in turn entails equally substantial energy consumption.

The report states that the surge in electricity demand is primarily driven by three factors: first, the accelerated replacement of traditional data centers by AI data centers; second, the sharp increase in power consumption of high-performance computing chips, such as NVIDIA’s Blackwell architecture, with its GB200 chip consuming up to 2.7 kilowatts—far exceeding previous generations; and finally, the continuously rising power density of server racks, with the report predicting that NVIDIA’s next-generation Rubin Ultra NVL576 architecture could have a rack thermal design power (TDP) of up to 600 kilowatts.

The report argues that compared to Europe and the United States, China holds advantages in terms of power reserves, cost, renewable energy supply chains, grid infrastructure, and equipment supply.

It is estimated that by 2025, China’s grid will have an effective reserve margin of approximately 30%, higher than less than 25% in the U.S. and about 15% in the EU. Additionally, China’s industrial electricity prices are 30-60% lower than those in the U.S. and EU, and its grid infrastructure is younger, with an average age of less than 20 years, compared to over 40 years in Europe and the U.S.

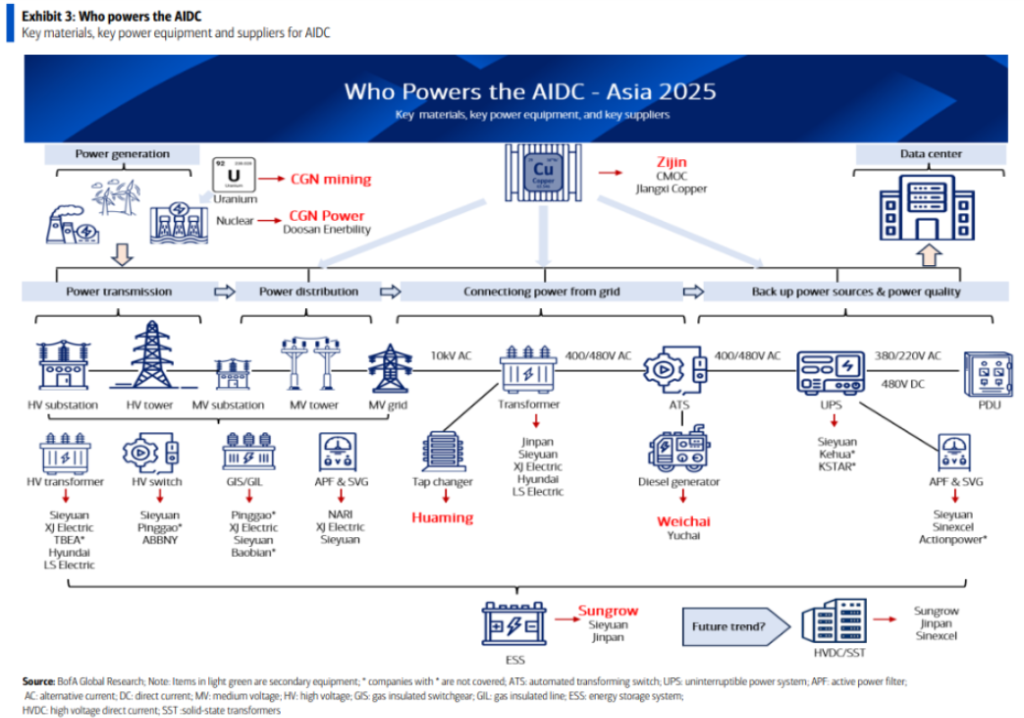

China’s power advantages pave the way for the development of AI data centers, thereby creating five major investment opportunities.

- Nuclear Power and Uranium: Due to its stable, efficient, and low-carbon characteristics, nuclear power has become an ideal baseload power source for AI data centers. The report predicts that by 2030, China’s installed nuclear power capacity will increase from 60 gigawatts (GW) in 2025 to 100 GW, accounting for 60% of global nuclear power capacity under construction. This will directly lead to a shortage of uranium resources and a rise in prices.

- Grid Equipment: Global grid upgrades and the additional load brought by AI are driving a surge in demand for key equipment such as transformers. Chinese suppliers, leveraging their robust supply chains and production capacity advantages, are well-positioned to fill the gap in the global market.

- Energy Storage Systems (ESS): ESS is essential for ensuring power stability. The report forecasts that the global new installed capacity of ESS will grow at a compound annual growth rate (CAGR) of 21% from 2024 to 2030, while the order growth rate for Chinese companies is expected to exceed 30%.

- Diesel Generators: As the last line of defense during data center power outages, diesel generators experience strong market demand. The report anticipates that the market CAGR will reach 28% from 2024 to 2027.

- Specialized Power Supplies: High-voltage direct current (HVDC) systems and power supply units (PSU) within AI servers are seeing rising value and technical requirements as chip power consumption grows exponentially.

Cooling AI: Surging Demand for Liquid Cooling Technology and Critical Metals

While high-performance chips deliver immense computational power, they also generate significant heat. The report highlights that every 10°C increase in server temperature may reduce equipment reliability by 50%. Consequently, efficient heat dissipation has become vital for AI data centers.

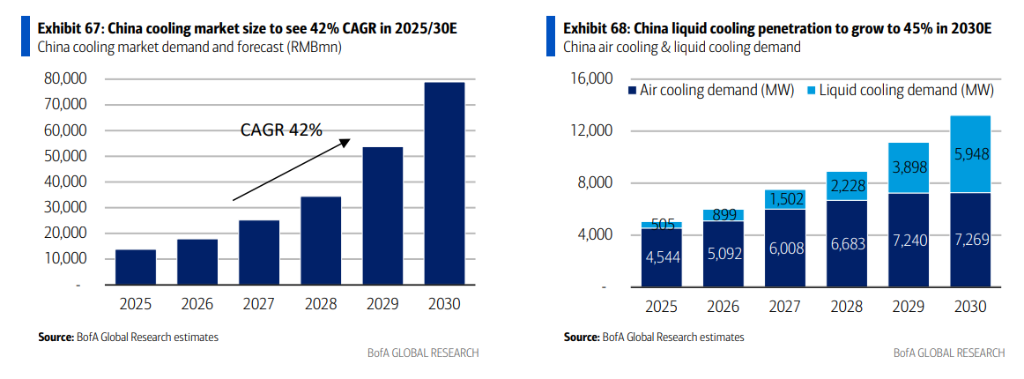

The report emphasizes that as the power density of AI servers surges, traditional air cooling technology can no longer meet the heat dissipation demands, making liquid cooling an inevitable choice.

Bank of America predicts that China’s liquid cooling market will expand at a CAGR of 42% from 2025 to 2030, with market penetration reaching 45% by 2030. Compared to traditional air cooling, liquid cooling offers 20-50 times higher heat transfer efficiency and can save up to 30% on electricity. Bank of America analysts note in the report that emerging technologies like immersion cooling are gaining increasing attention.

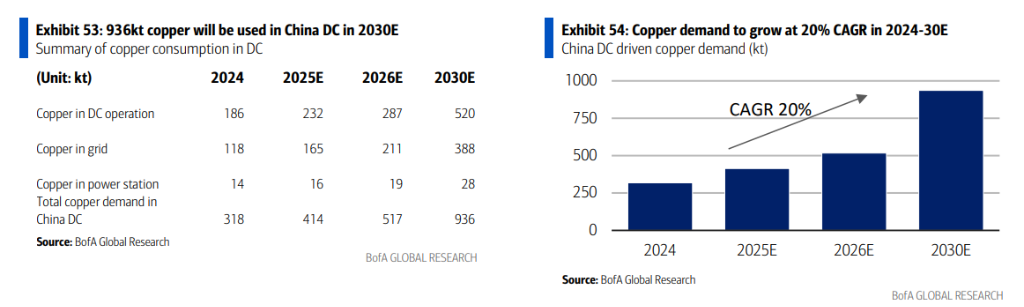

At the same time, the construction of AI data centers relies heavily on base metals such as copper and aluminum. For instance, copper plays a crucial role in power transmission, signal transmission, and thermal management.

- Copper: As a core material in power transmission and cooling systems, the demand for copper is expected to grow significantly. Bank of America predicts that by 2030, the direct copper demand driven by China’s AI data centers will increase to nearly 10 million tons, accounting for 5-6% of China’s total copper demand at that time. Additionally, indirect demand from power grids and electrical equipment will further amplify copper consumption.

- Aluminum: Equally important in structural components and cooling equipment for data centers. The report forecasts that by 2030, data centers will drive aluminum demand to 695,000 tons, representing a compound annual growth rate (CAGR) of 16% from 2025.

- Rare metals such as tungsten, tin, and gallium also play an indispensable role in chip manufacturing.

Construction Engineering: Building the Physical Foundation of the AI Era

Within the RMB 800 billion non-IT infrastructure market, engineering and construction (E&C) represents a critical segment. According to the report, construction engineering and related expenses account for up to 40% of the non-IT costs in data centers, making it the largest expenditure category after power systems.

This portion of investment is primarily driven by national strategic projects. The report specifically highlights China’s “East Data West Compute” initiative. The implementation of these large-scale projects directly translates into significant demand for civil engineering, building installation, and project management services. The construction of these data center clusters not only includes the physical buildings but also involves complex engineering tasks such as grid integration and fiber optic network deployment.

Bank of America’s report unveils a new landscape for investors amid the AI boom. Beyond the well-known semiconductor and software companies, a vast ecosystem comprising power, industrial, and materials companies is becoming an essential cornerstone of the AI era. The report suggests that leading enterprises in these sectors will benefit significantly.

This article is from the WeChat public account “Hard AI.” For more cutting-edge AI news, please visit here.